Future Pension Act: The consequences for your pension plan.

After years of discussion about the pension system, the Pension Deal is now almost complete. On 30 March 2022, the final legislative proposal for the Pension (Future) Act was sent to the House of Representatives. As soon as the House of Representatives and the Senate agree, we will have a new law that will significantly alter the current Pension Act. A lot is going to change. And that calls for a new look at your pension plan.

What does the new system entail?

At the heart of the new system is the abandonment of the system of pension promises. The familiar final-pay and averagepay pension plans with a view to fixed, guaranteed pension benefits on retirement date will disappear. In the new system, it is not the pension outcome but the contributions that take a central position. Pensions will fluctuate more in line with the investments of pension funds and insurers and will therefore become less certain. Companies that do not have a pension plan with a pension fund now often offer pension plans in the form of 'defined contribution plans'. In this type of arrangement, the premium is the starting point. Often the premium is based on the employee's age. The principle of agedependent premiums, the so-called contribution ladders, will be abolished. The new system is based on a fixed premium percentage that is determined by the employer.

Transitional law

As of 2023, transitional law will apply to employees in existing plans. In that situation, the contribution ladders may remain in place. Employees who enter service from 2027 onwards may no longer participate in a pension plan with contribution ladders. For them, the contribution percentage must remain the same. We call this a flat rate. If necessary, you can also introduce the new system earlier. If you opt for transitional law, the flat rate must be introduced simultaneously for new employees. Employers who opt for the transitional law will then have two pension plans.

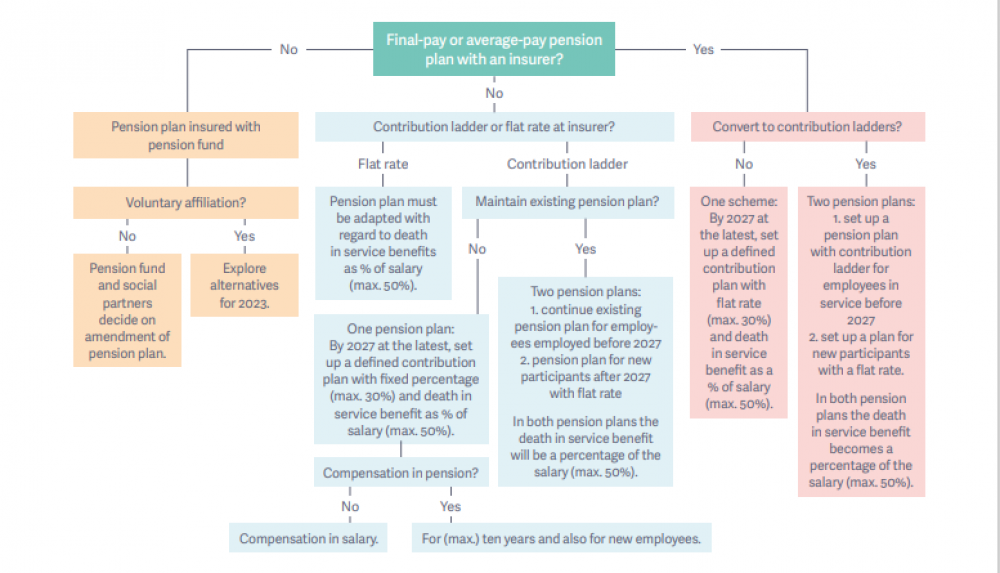

Modify plan

Employers who adjust their existing plan will be confronted with compensation requirements. Compensation can be both in salary and in pension; the diagram below illustrates this further. If the plan is adjusted, the employer must draft a transition plan including its adjustments and their consequences.

Timetable Pension Deal

• House of Representatives / March 2022

• Consultation on subordinate legislation / April 2022

• Debate in House of Representatives / after summer 2022

• Consideration by The Senate / fourth quarter 2022

• Intended entry into force / January 2023

• Deadline 2027 (transitional law until 2027)

What does this mean for you as an employer?

The way in which old-age pensions are accrued is changing fundamentally. Every pension plan in the Netherlands will eventually need to be adjusted. Not only the accrual of old-age pension will change, but other parts of the pension plan, such as the death in service benefit, will change as well. This is a large and complex operation. Every situation is different and there is no default solution. The choices to be made depend, among other things, on your desired policy on employment

conditions and your budget.

Mapping out the possibilities

To prepare you, we have outlined the options available to pension plans. Many details in implementation have yet to become clear. The legislation is not yet set in stone. You do not have to change your pension plan as of January 2023. In most cases, employers have until 2027. Please note: if you have a final-pay or average-pay pension plan with a pension fund and wish to switch to an contribution ladder, this must be arranged before 2023. This also applies to employers who do not yet have a pension plan and still want to commit to an increasing premium ladder.

Any questions?

Meijers will be happy to guide you through this transition. If you have any questions, please do

not hesitate to contact your pension specialist.